With hot tub prices today ranging anywhere from $5,000 to $20,000 and beyond, it’s important to understand what goes into the overall cost of a spa and what your payment options include. In this comprehensive guide, we’ll line out all factors and considerations of financing hot tub purchases.

Browse to a specific category by clicking on any of the quick links below:

Hot Tub Financing Options Overview

When it comes time to pay for your spa, it helps to know there are hot tub financing options beyond cash and credit. Not everyone has or is comfortable using a chunk of cash from their checking account to pay for a larger ticket item all at once. And credit cards typically come with hefty finance rates hovering around 20%.

Let’s take a quick look at the benefits to financing your spa purchase.

- Financing a hot tub makes your larger ticket purchase affordable.

- When financing and spreading out the costs over time, you can feel good about including your preferred features and accessories rather than settling for less.

- And of course, hot tub financing avoids depleting your checking or savings account.

Just as you would with a car purchase, it’s helpful when purchasing a spa to look at all the payment alternatives and ensure you’re making a smart choice for your own personal finances. These include home equity lines of credit (HELOCs), home equity loans, personal loans, and spa financing through your spa dealer.

Home Equity Lines of Credit (HELOCs)

What is a HELOC and how does it work? A home equity line of credit is essentially a loan that functions like a credit card. It’s set up as a revolving line of credit for a stated maximum amount you can draw from or up to, rather than giving you a fixed dollar amount from the outset. Offered by your lender, the HELOC uses equity in the home as collateral and can serve as a type of second mortgage.

What is a HELOC and how does it work? A home equity line of credit is essentially a loan that functions like a credit card. It’s set up as a revolving line of credit for a stated maximum amount you can draw from or up to, rather than giving you a fixed dollar amount from the outset. Offered by your lender, the HELOC uses equity in the home as collateral and can serve as a type of second mortgage.

Since the balance on a HELOC can vary from day to day, the interest is calculated daily instead of monthly. There are two time-frames to be aware of with HELOCs: the draw period when funds from the loan are available for withdrawal and the repayment period when the draws taken must be repaid. It’s important to identify both so you know when interest is accruing and how long you have to spread out the costs of your purchase.

HELOCs are ideal for helping fund home improvement projects that come up, like adding a place to relax, rejuvenate, and unplug in your backyard. These lines of credit allow you to draw and pay interest only on the amount you use and the interest is tax deductible. The upfront costs are typically low and some HELOCs can be converted into fixed-rate loans if your improvement project becomes grander in scheme.

To get a HELOC, you apply through your home mortgage lender. The process is similar to getting a mortgage–the lender will want to know your employment and income details and current recurring expenses, along with the value of and equity in your home.

Home Equity Loans

How are home equity loans different from home equity lines of credit? Home equity loans are similar to HELOCs in that you’re still using equity in the home as collateral to secure the loan. But as you’d guess, this is a more conventional loan with a fixed funding amount that’s repaid in equal monthly installments over a set period of time.

Again, good for intermittent needs like home improvement project, a home equity loan acts much like a second mortgage with similar rates and can be secured through your mortgage lender as well as other lenders, banks, or credit unions. Be aware that these loans may have closing costs associated with them just as a mortgage does.

Advantages of home equity loans for spa finance typically include lower interest rates as compared to credit cards and other loan types (since they’re closer to actual mortgage rates), longer terms like mortgages, and the ability to borrow greater sums as long as you have the equity to cover it.

Personal Loans

A personal loan is simply money borrowed from a lender that’s repaid with interest in monthly installments over a set time period without anything but your credit to secure it. Personal loans generally have fixed-rates dependent on your credit score and history and offer another option for new or unanticipated events, as many home improvement projects turn out to be. You can apply for these loans through most financial institutions like banks and credit unions in addition to more non-traditional lenders online.

Since personal loans don’t involve your home and home equity, the main advantage they offer is easier application and speedier processing time. Whereas a home equity loan approval can take weeks, personal loans can often be secured in a matter of a day or two. The trade-off here is that rates on a personal loan tend to be quite a bit higher–somewhere in the middle of home equity loan and credit card rates.

Since personal loans don’t involve your home and home equity, the main advantage they offer is easier application and speedier processing time. Whereas a home equity loan approval can take weeks, personal loans can often be secured in a matter of a day or two. The trade-off here is that rates on a personal loan tend to be quite a bit higher–somewhere in the middle of home equity loan and credit card rates.

One established online lending provider who offers specific hot tub financing is Lightstream.com. For buyers with good credit, Lightstream offers competitive rates and doesn’t charge extra fees. Same-day funding is possible, and there’s even the option of choosing a different funding date so you can offset the timing to match your hot tub financing schedule.

If you are working on building your credit score and don’t necessarily qualify for a good or high credit score loan, there are still options available. The interest rates on a no, low, or bad credit loan, however, will be higher and the total funds offered may be less. The good news with these loans is that they not only help with spa finance, they help build your credit score provided you keep up with making your payments in full and on time each month.

Hot Tub Dealer Financing

It turns out that many hot tub dealerships have relationships with lenders or a lending program so they can offer hot tub financing directly to their customers. Just like auto dealerships, spa retailers’ rates can start at 0% and go up from there. Dealers frequently tie in special hot tub financing terms to periodic in-store promotions, which occur around certain holidays and events. For more on when to look for these special promotions, see Best Time to Buy a Hot Tub below.

The are two primary advantages when you finance hot tubs through the dealer: 1) simplification of the purchase process and 1) convenience–everything goes through one source and gives you an immediate response about approval. Dealers who offer financing for hot tubs work through financial institutions or their manufacturers who have established hot tub financing programs with reputable lenders. Even if you’re not buying during a spa financing promotion, their rates are generally competitive or better than personal loan rates offered outside the dealership.

Hot Tub Financing Comparison Table

| Interest | Terms | Approval Time | Collateral | |

| HELOC | ~5% | variable | 1-3 weeks | home |

| Home Equity Loan | ~5% | fixed | 1-3 weeks | home |

| Personal Loan | 10-25% | fixed | 1-2 days | credit |

| Dealer Financing | 0-10% | fixed | same day | credit |

Monthly Payment Examples when Financing a Hot Tub

While hot tub financing terms and offers will vary from one loan to the next, it’s useful to have a general idea of what your spa finance payments may look like. So let’s take a look at a few scenarios with different amounts borrowed, different interest rates, and different terms.

1. Amount financed: $7,000

- At 0% APR for 36 months, your monthly payment would be $195.

- At 5% APR for 36 months, your monthly payment would be $210.

- At 10% APR for 36 months, your monthly payment would be $226.

- At 15% APR for 36 months, your monthly payment would be $243.

2. Amount financed: $10,000

- At 0% APR for 48 months, your monthly payment would be $209.

- At 5% APR for 48 months, your monthly payment would be $231.

- At 10% APR for 48 months, your monthly payment would be $254.

- At 15% APR for 48 months, your monthly payment would be $279.

3. Amount financed: $13,000

- At 0% APR for 60 months, your monthly payment would be $217.

- At 5% APR for 60 months, your monthly payment would be $246.

- At 10% APR for 60 months, your monthly payment would be $277.

- At 15% APR for 60 months, your monthly payment would be $310.

What to Avoid when Financing a Hot Tub

Of course, you want to avoid the obvious pitfalls when you’re navigating the methods of spa finance: not considering all your options, misrepresenting your income when applying, and missing payments. But there are other tips you’ll want to be just as aware of.

Unfortunately, the business of lending includes scammers and predatory providers particularly online. To avoid getting involved with one of them, it’s important to do your due diligence when making a selection. Here’s what you want to watch for.

You don’t want a lender who:

- Isn’t registered to do business in your state.

- Doesn’t report to the major credit bureaus.

- Doesn’t readily disclose fees and terms.

- Requires upfront fees prior to funding the loan.

- Doesn’t have a safe, secure website.

When you start looking at lenders, the first thing to check on is where they’re registered to do business. This info can easily be found on your state’s financial institution regulatory bureau website. You’ll also want to make sure they report to the major credit bureaus, especially if you’re wanting to improve your credit score.

It’s also important that the rate, fees, and loan terms are clearly stated. This often means reading the fine print to make sure there aren’t any surprises that pop up during the lifetime of the loan. No reputable lender will ask for fee payment before you receive loan funds. Many incorporate their fees into the loan itself to avoid any extra upfront and/or closing costs.

Lastly, make sure your privacy and security will not be an issue. If you’re using an online lender, their website should start with “https” instead of “http.” This is the current standard for ensuring your personal information won’t be hacked or compromised.

Best Time to Buy a Hot Tub

As mentioned above, spa dealers have consistent times of the year when they host sales events with special discounts and promotions for the consumer. The most common sales periods occur when they’re trying to move inventory quickly, usually when they’re about to get new models in.

Hot tub manufacturers typically work on a calendar year, releasing new models in January. So dealers will often offer deep discounts late in the year (December) and at the very beginning of the year. Otherwise, holidays like Memorial Day and Labor Day tend to be popular times for dealer sales events.

You can learn more about when and where to look for the best hot tub sales and promotions with this article on Best Time of Year to Buy a Hot Tub.

Installation Costs

When talking about hot tub financing, it helps to know what the total costs of your hot tub purchase are going to be in order to secure the right amount of funding. In this comprehensive guide on financing a hot tub, we’ll break down all potential costs a buyer may need to put together a working budget. Let’s start with pre-purchase installation costs.

Foundation

An average 7 ft x 7 ft hot tub weighs in around 700-800 pounds dry and holds over 325 gallons of water. Needless to say, you want to make sure what you’re setting the spa on top of is strong enough to hold it. An inadequate foundation, particularly one that isn’t completely flat, can lead to damage as well as a voided hot tub warranty.

If you’re not placing your spa on an existing patio or deck, one of several other foundation or flooring options is recommended. These include different forms of concrete as well as crushed rock or gravel. While concrete slabs or pads tend to be most common, pavers and bricks can offer a more decorative look if you’re wanting to elevate your space in terms of style and design. Please note that concrete foundations should be a minimum of 4 inches thick, reinforced with either rebar or mesh, and attached to bond wire for electrical grounding purposes.

Crushed rock is another alternative and can prove to be a cost-effective one at that. The recommended thickness of a crushed gravel bed is also at least 4 inches–this should be measured after compacting to avoid settling of the hot tub once in place. Because it doesn’t compact as well, pea gravel is not a good option and should be avoided as a spa foundation option.

For 10’x10’ foundation, costs vary according to material:

- Concrete pad ($6/sq ft): $600

- Concrete pavers ($10/sq ft): $1,000

- Concrete bricks ($9/sq ft): $900

- Crushed rock/Gravel ($1.50/sq ft): $150

Electrical

When considering placement of your hot tub, you want to select a location within reach of a power source and with access to a proper drain or outdoor drainage area. Also make sure you have the proper wiring in place prior to installation. It’s a good idea to check with both local and national wiring rules and a licensed electrician for logistical advice and requirements specific to your area. As you’re finalizing your spa’s location, be sure that the spa is positioned so access to the equipment compartment will not be blocked.

The two electrical needs you’ll need within reach of your spa are: 1) a 240 volt panel with GFCI protection and 2) a circuit breaker.

- 240 volt 50 AMP panel with neutrally protected GFCI: $1,000 (additional cost for longer distances from panel to hot tub)

- 50 AMP breaker: $200

Hot Tub Pricing (with accessories & delivery included)

Chances are if you’re thinking about purchasing a spa but are having a hard time pinning down actual costs associated with the hot tub purchase. Because hot tub prices are still set at the local level, manufacturers don’t typically publish list prices on their products. Though you may not be able to get specific on the price for every model in every configuration without a visit to your local Authorized hot tub dealer, you can get a reasonable estimate on how much adding a hot tub to your home will end up costing in the long run.

Most moderate to high-end hot tubs are built by top manufacturers with quality acrylic shells and well-built frames and cabinets. Consider things like how well the hot tub is engineered, what materials it uses, what jet technology is used, where it’s made (USA and Canada), what equipment like pumps and heaters are used, and the overall reputation of the company. In doing so, you can determine which hot tubs offer the best value. Where a specific hot tub falls in this price range depends primarily on the extent of optional features chosen. For instance, Bullfrog’s A series and STIL models fit this category.

Most moderate to high-end hot tubs are built by top manufacturers with quality acrylic shells and well-built frames and cabinets. Consider things like how well the hot tub is engineered, what materials it uses, what jet technology is used, where it’s made (USA and Canada), what equipment like pumps and heaters are used, and the overall reputation of the company. In doing so, you can determine which hot tubs offer the best value. Where a specific hot tub falls in this price range depends primarily on the extent of optional features chosen. For instance, Bullfrog’s A series and STIL models fit this category.

Top quality hot tub manufacturers commonly offer a budget to mid-price spa line as well. These spas have fewer features and less complete hydrotherapy options but still offer good reliability and comfort. To determine value in this range, look for an established brand, established dealer or sales channel, positive consumer feedback, along with manufacturing in the USA or Canada. Bullfrog’s X and R Series are good examples in this range.

Manufacturers do make entry-level spas in the <$6,000 range, but it’s wise to beware. Many spas in this price range are made using methods that produce a limited usable life product with poor materials and workmanship from knock-off overseas companies. And many cost considerably more to operate. For high-quality, entry-level spas, look for those same established higher quality manufacturers as mentioned above.

Keep in mind that these are outdoor hot tubs. They are exposed to environmental factors every day, all day. A well-built hot tub will last much longer than a poor quality spa, often a decade or more. This means your initial purchase price will be spread over more years of use.

- Swim Spa: $25,000 – $40,000

- Elite Luxury: $20,000 – $25,000 with 10+ year life expectancy

- Luxury: $15,000 – $20,000 with 10+ year life expectancy

- Mid-Range: $10,000 – $15,000 with 10+ year life expectancy

- Value: $5,000 – $10,000 with 8-10 year life expectancy

- Entry-level: $2,000 – $5,000 with 8-10 year life expectancy

It’s no secret that hot tubs are a larger ticket-priced product. So it makes sense that you’ll want to own yours for as long as possible. When you decide to go with a top quality spa, engineered to last, you will have on-demand hydrotherapy, relaxation, and fun right in your own backyard. No other product offers as many health and lifestyle benefits.

So, consider the quality and value first when making your decision on which hot tub is best for you. Your purchase price may be a little higher, but you’ll be rewarded with better features, better hydrotherapy, and a lower cost of ownership over time.

Trade-in and Used Hot Tub Considerations

Do you currently have a hot tub you’re looking to upgrade? The benefits of trading up are plenty: a more personalized experience, more powerful performance, savings on energy costs, and updated technology to name a few. It’s worth it to ask your local hot tub dealer if they have a trade-in program so you can reap these benefits sooner rather than later. Retailers oftentimes take your used spa and apply a trade-in discount to your new hot tub purchase. They may even include pick up and disposal services, making the transition from old to new a seamless one for you.

If you’re considering buying a used hot tub rather than new, read this article Should I Buy a Used Hot Tub? first to make sure it’s the right decision for you.

Ownership Costs

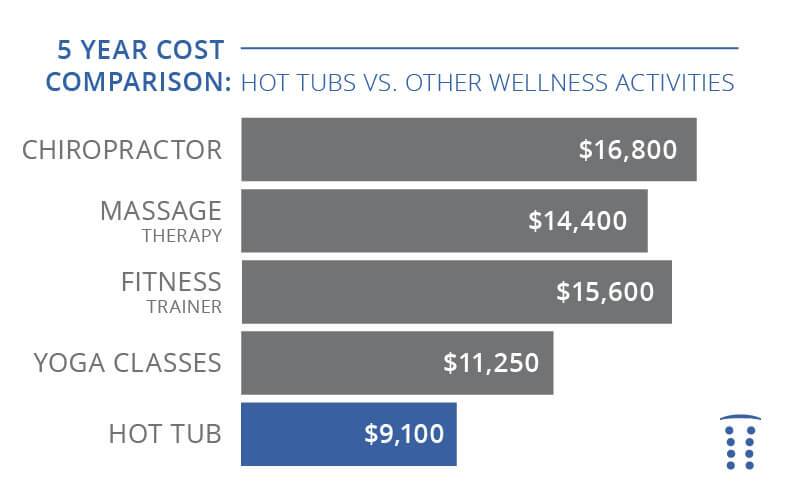

Are you wondering how much a hot tub will cost over its lifetime? Before going into specific costs, it’s helpful to compare ownership costs to other expenditures you might make in place of a hot tub. Alternative solutions to getting relief from your aches and pains, the stress of the day, and feelings of disconnection include massage therapy, chiropractor visits, fitness training, and yoga classes. Here’s how each of these adds up over 5 years:

As you can see, the stats show that a hot tub purchase will cost much less over its lifetime as compared to other recovery and rejuvenation options.

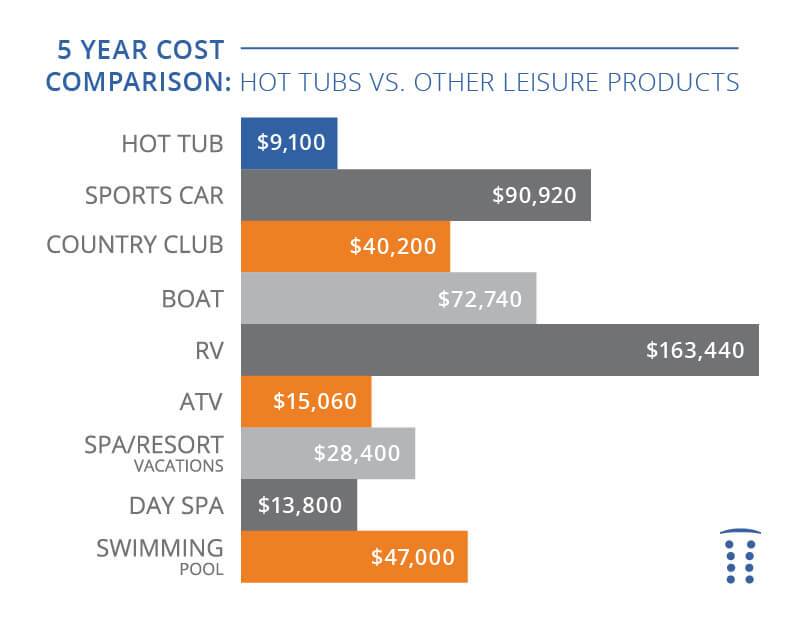

But what about comparing ownership costs to those of more general recreational or leisure products? We also have a 5-year cost comparison between a hot tub purchase and a sports car, country club membership, boat, RV, ATV, resort vacation, day spa visits, and swimming pool.

Now we’ve established that the hot tub purchase easily qualifies as a smart investment, the question becomes “What do we mean by ownership costs?” To get a better idea, let’s take a look at a hot tub’s operational and maintenance costs you can expect once your hot tub is up and running.

Cover and Filter Replacement

Because they’re exposed to the environment every day, all day, covers tend to wear out and need replacement about every 4 to 6 years. It’s recommended that filters are changed every 12 to 24 months.

- Cover Replacement Cost: $500 each

- Filter Replacement Cost: $45 each

Energy Usage

High-quality spas are usually full-foam insulated except for the area where pumps and heaters are located. This helps to isolate the hot water in the spa from the cold and keep warmth within. Full-foam insulated spas require much less energy to keep them ready to use.

One way to find energy efficient hot tubs is to look at the data compiled by the California Energy Commission, which keeps hot tub energy use statistics. Pay attention to the spa brands that consistently show at the top of these lists.

Here are monthly energy use costs of comparable 7 foot hot tub models among the major brands. These costs are based on data published by California Energy Commission and estimated at $0.10 per kilowatt-hour (local rates vary).

- Bullfrog Spas: $11.81 per month

- Hot Spring®: 12.60 per month

- Caldera Spas®: $16.49 per month

- Sundance®: $18.15 per month

- Jacuzzi®: $18.80 per month

For a more in-depth look at how energy efficiency works in a hot tub and what to look for when buying, check out this video What Makes a Hot Tub Energy Efficient and our article on Most Energy Efficient Hot Tubs vs Less Energy Efficient Hot Tubs.

Chemical Maintenance

In order to maintain clean water so it’s ready to use at any time, regular use of these items is commonly required to balance spa water: test strips, pH Increaser, pH Decreaser, bromine sanitizer, chlorine sanitizer, oxidizer, and anti-foam treatment. Water should be tested at least every time the spa is used. Of course, the cost of maintenance supplies depends on frequency and volume of use (how often and how many people), so it can vary from one owner to another.

- High Use: $40 per month

- Average Use: $30 per month

- Low Use: $20 per month

Our comprehensive Hot Tub Water Care Guide offers additional insight and tips to maintaining your spa’s water balance and overall health.

Hot Tubs and Home Value

It’s always wise to consider the return on investment when taking on a home improvement project. A hot tub purchase alone, particularly a portable spa that can be moved from one home to another easily, doesn’t always add value. But there are occasions when a hot tub can in fact impact your home’s worth.

It’s always wise to consider the return on investment when taking on a home improvement project. A hot tub purchase alone, particularly a portable spa that can be moved from one home to another easily, doesn’t always add value. But there are occasions when a hot tub can in fact impact your home’s worth.

When you build your spa into the backyard environs with a designated space or structure to house it, you will typically get a return on your investment. Landscaping around the hot tub also helps, plus it improves the overall experience while you’re still the owner and primary user.

You can find additional info on how a hot tub can increase the value of your home in our article Home Improvement: Does an Outdoor Hot Tub Increase the Value of Your Home?.

Become a Hot Tub Expert

Subscribe to learn more about either buying or maintaining a hot tub and we’ll send you everything you need to know.